SmartSkor: Forward-Looking Equity Ranking

SmartSkor is our primary equity-ranking framework. It periodically analyzes 100+ factors spanning value, momentum, profitability, attention, fundamental momentum, and investment categories.

The resulting composite SmartSkor forecasts the risk-adjusted performance ranking of a security over the next month. The SmartSkor framework is best utilized through model portfolios rather than concentrated bets on few securities.

The resulting composite SmartSkor forecasts the risk-adjusted performance ranking of a security over the next month. The SmartSkor framework is best utilized through model portfolios rather than concentrated bets on few securities.

How does SmartSkor help?

SmartSkor combines multiple factors, each capturing a different source of market inefficiency

No single factor works all the time. Combining them creates a more reliable signal

More predictable stocks

Optimally investing firms

Beyond conventional metrics

Firms on a steady uptrend

Strong fundamentals

Not hyped

Undervalued companies

Better Stock Selection

Reduced Biases

Better Performance

SmartSkor Methodology

Our systematic security analysis approach has four stages

01

Test the efficiency of existing cross-sectional characteristics

Replicate decades of financial economics research and backtest the economic and statistical significance of firm characteristics and their ability to predict future stock performance.

02

Conduct original research to identify new firm characteristics

Use economic theory and original hypotheses to identify new firm characteristics that improve return predictability. Backtest the efficacy of these new characteristics in the presence of existing ones.

03

Create model portfolios using SmartSkors

Construct model portfolios based on different risk, investment and industry preferences using firms with the highest SmartSkor values, i.e., values of 10.

04

Rebalance portfolios on a periodic basis

Firm level SmartSkors change in regular, pre-scheduled intervals. This is reflected in the composition of model portfolios as firms with lower SmartSkors are replaced by firms with higher SmartSkors periodically in each model portfolio.

Benefits

SmartSkor’s design deliberately penalizes variables associated with mispricing and sentiment

High volatility, idiosyncratic distress, or excessive retail attention reduce the composite, while profitability, transparency, and disciplined investment increase it.

The result is an ex-ante ranking of securities by expected return, rooted in evidence and invariant to market narrative.

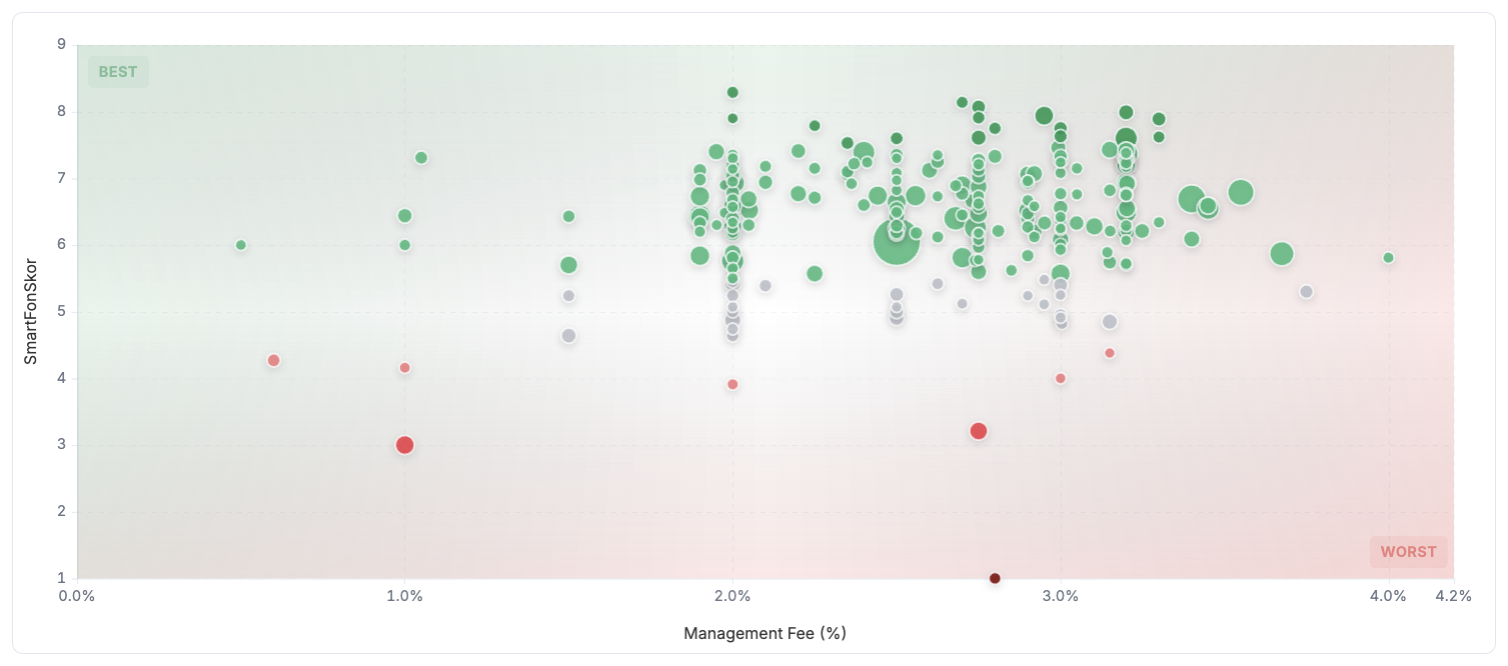

SmartFundSkor

SmartFundSkor: Bottom-Up Fund Evaluation

SmartFundSkor extends the same logic to the portfolio level

For each equity fund, the system computes a holdings-weighted average of underlying SmartSkors, adjusted for turnover and concentration. The score reflects the expected risk-adjusted performance of the fund’s current positions, not its historical returns.

In addition, we provide investors with over a dozen professionally designed model portfolios that help them capture the full power of SmartSkor according to their individual investment preferences, risk tolerance, and portfolio objectives.

In addition, we provide investors with over a dozen professionally designed model portfolios that help them capture the full power of SmartSkor according to their individual investment preferences, risk tolerance, and portfolio objectives.

Turn insights into profitable investment decisions with SmartSkor

Move beyond historical rankings, invest based on the forward-looking

quality of publicly traded equities.

value

attention

momentum

fundamental

momentum

momentum

investments

profitability