Empowering Retail Investors, Tools for Success: Would you want a personalized assessment?

Empowering Retail Investors, Tools for Success: Would you want a personalized assessment?

Empowering Retail Investors: Tools for Success

The financial industry has spent decades trying to improve investor outcomes.It has built sophisticated risk models, launched financial literacy campaigns, created index funds, and deployed robo-advisors. All of these have delivered genuine value. Yet the core problem persists: the typical retail investor continues to underperform a passive benchmark — not marginally, but substantially and consistently.

What has been missing is not better products in the traditional sense. It is a different kind of infrastructure: one that works on the investor rather than just for the investor. This post describes what that looks like in practice —the tools, the logic behind them, and the evidence that they can make a measurable difference.

Why Education Alone Has Not Been Enough

The standard response to investor underperformance is education. Teach people about diversification, explain the dangers of market timing, publish articles on behavioral bias, and — the thinking goes — investors will make better decisions.

The evidence does not support this optimism. Financial literacy programs consistently show that increased awareness does not reliably translate into improved trading behavior. An investor who understands the disposition effec tintellectually can still fall prey to it emotionally when confronted with a stock sitting at a 30-percent paper loss. Knowledge and action are not the same thing. Behavioral inertia, framing effects, and the desire for control mean that even well-informed investors make predictable mistakes under pressure.

The implication is not that education is useless — it is that education is insufficient on its own. What changes behavior at scale is not information delivered in the abstract, but feedback delivered at the moment of decision, grounded in the investor's own history, and actionable in real time.

The Behavioral Report Card: Turning Self-Knowledge Into an Edge

The starting point for any meaningful intervention is an accurate diagnosis. The Behavioral Report Card is designed precisely for this purpose: it analyzes an investor's complete trading history and portfolio composition to produce quantitative, personalized scores across the key dimensions of behavioral bias.

These dimensions — under-diversification, disposition effect, overconfidence and excessive turnover, lottery stock preference, attention chasing, and home bias — are not abstract categories. They are empirically documented patterns with measurable impact on returns. In our own analysis of retail trading data, investors in the lowest quintile of behavioral bias earned approximately one percentage point more in market-adjusted returns over a 30-day period than investors in the highest quintile. Compounded across years of trading, this gap becomes transformative.

The Report Card does not simply name a bias. It contextualizes it. An investor who scores poorly on diversification sees their actual Sharpe ratio compared against the market, a simulation of how much risk they are bearing unnecessarily, and — critically — concrete suggestions for which securities, added at what weight, would most efficiently reduce that concentration while increasing expected return.

An investor flagged for disposition bias sees a counterfactual: what would the portfolio value be today if, in each instance where a winner was sold early or a loser held too long, the opposite decision had been made? This is not a lecture about cognitive psychology. It is a personalized, data-grounded estimate of what the bias has cost in real money.

An investor showing lottery preference sees the probability distribution of outcomes from the high-skew stocks they favor, computed from historical return distributions. The message is not "this is risky" — it is "based on the actual data for securities like this one, the probability of generating a return above the market over the next 12 months is less than one in ten."

**A note on early access.** The fully automated Behavioral Report Card is currently in development. In the meantime, TuneUp is offering a personalized version directly: investors who share one to five years of past trade history with us receive ahand-crafted Report Card built from the same methodology, applied to their own data by our research team. If you are curious what your behavioral profile looks like — what your biases have cost you and where the clearest room for improvement lies — this is the place to start. Reach out to us to submit your trading history and we will take it from there.

Interventions at the Moment of Decision

Behavioral diagnostics matter most when they arrive in context — not in amonthly report reviewed after the fact, but at the exact moment a consequentialdecision is being made.

Real-time intervention is the second pillar of the empowerment framework. Whenan investor is about to execute a sale on a stock that has risen 40 percentsince purchase, the system can surface the relevant evidence immediately: thehistorical pattern for this investor's prior sales of winning positions, theaverage subsequent performance of those securities, and the current SmartSkorranking for the stock in question. If the evidence suggests the stock still hashigh expected returns, the investor receives a clear, calibrated recommendationto reconsider — not as a command, but as a structured data point.

Similarly, when an investor places a large buy order in a stock that is tradingmat the highest attention levels in its sector — high recent volatility,elevated search volume, significant short-term price momentum — the intervention surfaces the statistical profile of that cohort of securities:their expected return, their historical volatility, and the typical outcome forinvestors who have made similar trades in similar conditions. The goal is notto override the investor's judgment. It is to ensure that judgment is operatingwith the full picture.

This kind of point-of-decision intervention is qualitatively different from education, and qualitatively different from automation. The investor retains full agency. What changes is the quality of information available at the moment the decision is made.

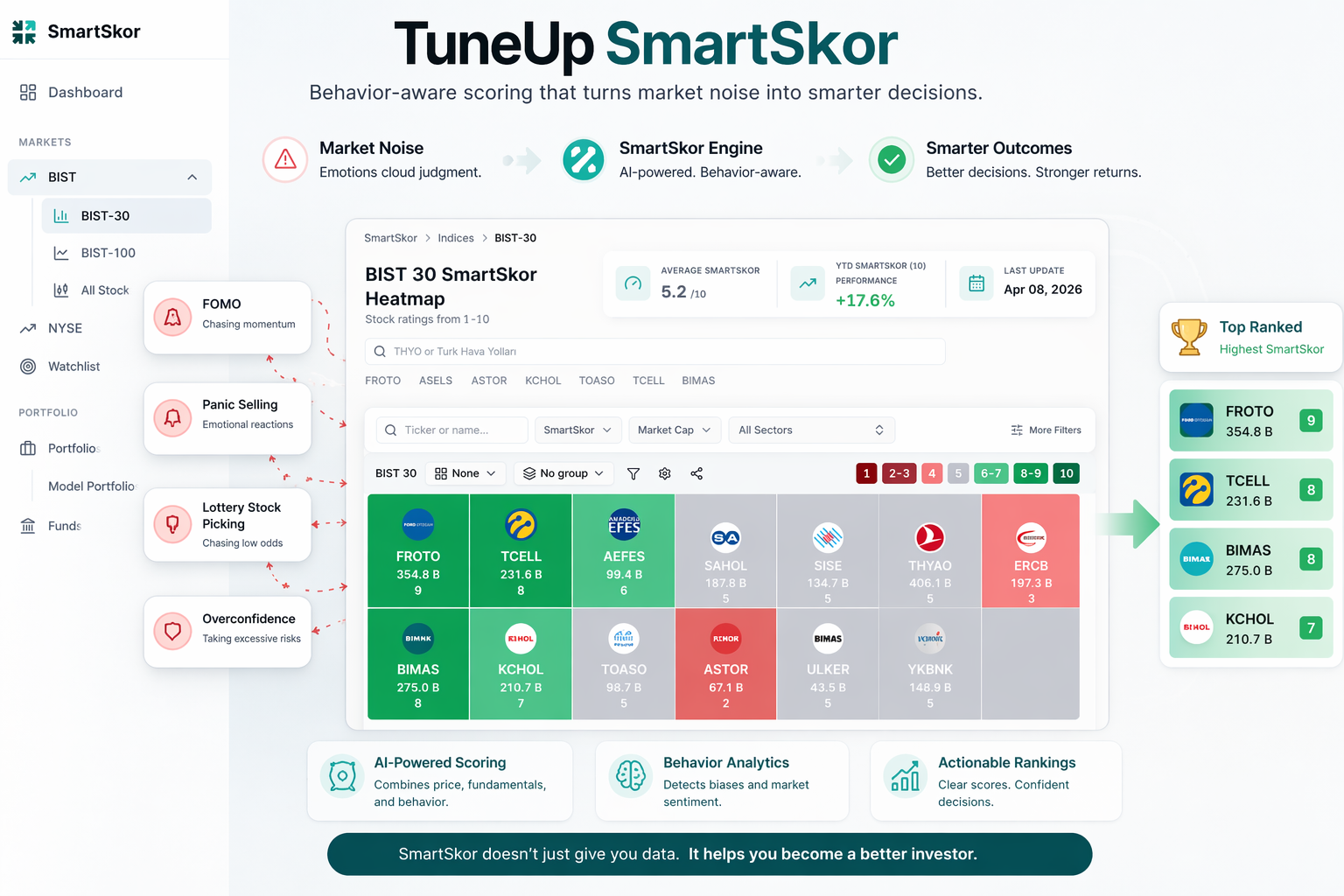

The SmartSkor Connection: Making Recommendations Actionable

Similarly, when an investor places a large buy order in a stock that is tradingmat the highest attention levels in its sector — high recent volatility,elevated search volume, significant short-term price momentum — the intervention surfaces the statistical profile of that cohort of securities:their expected return, their historical volatility, and the typical outcome forinvestors who have made similar trades in similar conditions. The goal is notto override the investor's judgment. It is to ensure that judgment is operatingwith the full picture.

This kind of point-of-decision intervention is qualitatively different from education, and qualitatively different from automation. The investor retains full agency. What changes is the quality of information available at the moment the decision is made.

Behavioral feedback is most powerful when it is accompanied by a viable alternative. When the Report Card identifies that an investor's portfolio isoverly concentrated in lottery-type stocks, it is not sufficient to say"this is suboptimal." The investor needs to know: what should I hold instead?

This is where SmartSkor integrates directly with the behavioral toolset. Forany investor flagged on diversification, the system recommends specific securities with two properties: low correlation with the existing portfolio andhigh SmartSkor rankings. For any investor flagged on lottery preference, the recommendation is a security in the same sector with lower idiosyncratic riskand a better expected-return profile. For any investor whose buy decisions haveconsistently underperformed, the system makes direct stock recommendations based on current expected-return rankings — stocks the data suggests theyshould be considering but are not.

This closes the loop between diagnosis and action. The investor does not justlearn that they are biased; they receive a concrete, evidence-based path towarda better portfolio.

The Return on Better Behavior

The empirical case for these tools is not speculative. From our own data, wecan quantify the relationship between behavioral bias and trading outcomes with unusual precision.

The returns following investor purchases in our dataset significantly underperformed the market — not slightly, but by 3 to 6 percent over a 90-daywindow. The stocks investors sold subsequently outperformed. The highest-bias quintile of investors underperformed the lowest-bias quintile by nearly one percentage point per month. And critically: a 1-percent improvement in market-adjusted returns was associated with approximately 0.25 additional trades per quarter — meaning better outcomes translate directly into more engagement, more retention, and a more active investor base.

This last point matters commercially as well as ethically. An investor who earns better returns stays in the market longer, trades with more confidence, and builds a more constructive relationship with their broker or platform. Reducing bias is not a cost imposed on a business — it is a compounding returnto one.

A Different Model of Financial Empowerment

The dominant model of retail financial empowerment has been informational: give people access to data, research, and tools, and trust that they will use them well. The evidence suggests this model is necessary but not sufficient. Information that arrives too late, in the wrong format, or without an actionable recommendation does not change decisions.

The alternative is a model that is simultaneously diagnostic, contextual, and constructive — one that tells investors where they are going wrong, shows themin their own data what it has cost, and offers a specific, evidence-grounded next step. That is what the combination of the Behavioral Report Card, real-time intervention, and SmartSkor-based recommendations is designed to deliver.

Empowerment, properly understood, is not the same as information access. It is the capacity to act more rationally than you otherwise would — to be better than your own defaults. Building that capacity, at scale, for the investors whoneed it most, is what this tool set exists to do.

*The Behavioral Report Card and SmartSkor recommendations are core products ofTuneUp Fintech, developed from peer-reviewed research in behavioral finance andempirical asset pricing.*

Turn insights into profitable investment decisions with SmartSkor

Move beyond historical rankings, invest based on the forward-looking

quality of publicly traded equities.

momentum